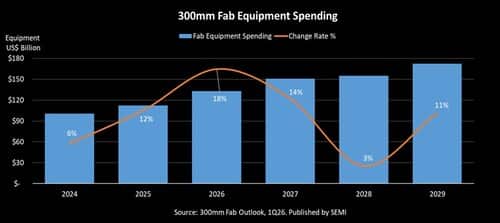

Global spending on 300mm semiconductor fabrication equipment is set to witness sustained double-digit growth through 2027, according to the latest outlook released by SEMI. The report projects worldwide investment to rise 18% to $133 billion in 2026, followed by a further 14% increase to $151 billion in 2027, marking a historic expansion in manufacturing capacity.

The growth trajectory reflects the accelerating demand for artificial intelligence (AI) chips across data centers and edge computing applications, alongside increasing global efforts to localize semiconductor supply chains. According to SEMI, these factors are reshaping investment priorities and driving unprecedented capital commitments across the industry.

Looking ahead, the momentum is expected to continue, albeit at a moderated pace. Global 300mm fab equipment spending is forecast to grow 3% to $155 billion in 2028 and rise another 11% to $172 billion by 2029, indicating a sustained long-term investment cycle.

Industry leaders note that AI is fundamentally altering the scale and pace of semiconductor manufacturing investments. As demand intensifies for high-performance and energy-efficient chips, manufacturers are accelerating capacity expansion, particularly in advanced nodes.

The logic and micro segment is projected to lead equipment spending, with investments expected to reach $228 billion between 2027 and 2029. This growth is largely driven by foundry demand for cutting-edge technologies, including sub-2nm nodes. These advanced processes are critical for enabling the performance gains and efficiency required for next-generation AI workloads. At the same time, demand across mature nodes is expected to remain stable, supported by a broad range of electronic applications.

The memory segment is also entering a new growth phase, with total equipment spending projected at $175 billion over the same period. Within this category, DRAM is expected to account for $111 billion, while 3D NAND is forecast to reach $62 billion. The surge in memory demand is closely linked to AI workloads, where training processes require high-bandwidth memory (HBM), and inference applications drive demand for large-scale data storage solutions.

SEMI noted that AI-driven demand is helping to stabilize the traditionally cyclical memory market by sustaining high levels of investment across the supply chain. This shift is expected to mitigate volatility and support long-term growth.

Regionally, investment is expected to remain widely distributed across major semiconductor manufacturing hubs. China, Taiwan, South Korea, and the Americas are projected to account for the bulk of spending between 2027 and 2029, driven by a combination of advanced-node expansion and memory capacity upgrades.

China’s investment is expected to remain strong due to ongoing domestic capacity expansion and national initiatives aimed at strengthening semiconductor self-reliance. Taiwan is likely to focus on leading-edge foundry capacity, particularly in 2nm and sub-2nm technologies, while South Korea’s outlook is closely tied to memory sector growth. In the Americas, investment will be supported by efforts to expand advanced manufacturing and reinforce domestic supply chains.

Other regions, including Japan, Europe, the Middle East, and Southeast Asia, are also expected to see steady growth, supported by government incentives and strategic initiatives aimed at enhancing supply chain resilience.