Global semiconductor revenues have crossed the $300 billion threshold in the first quarter of 2026, extending a powerful industry upswing driven by artificial intelligence demand and an unprecedented surge in memory pricing, according to new data from Omdia.

The market generated $319 billion in revenue in 1Q26, a 27% increase from the previous quarter. The expansion marks the strongest quarter-on-quarter growth since Omdia began tracking the sector in 2002. It also extends a rare streak of three consecutive quarters of double-digit gains, with another rise expected in the current quarter.

The industry is now tracking toward more than $700 billion in revenue in the first half of 2026, reinforcing expectations that semiconductors are entering one of their most expansionary cycles on record. The rally has been anchored by sustained demand for AI infrastructure, hyperscale data centers, and high-bandwidth computing systems.

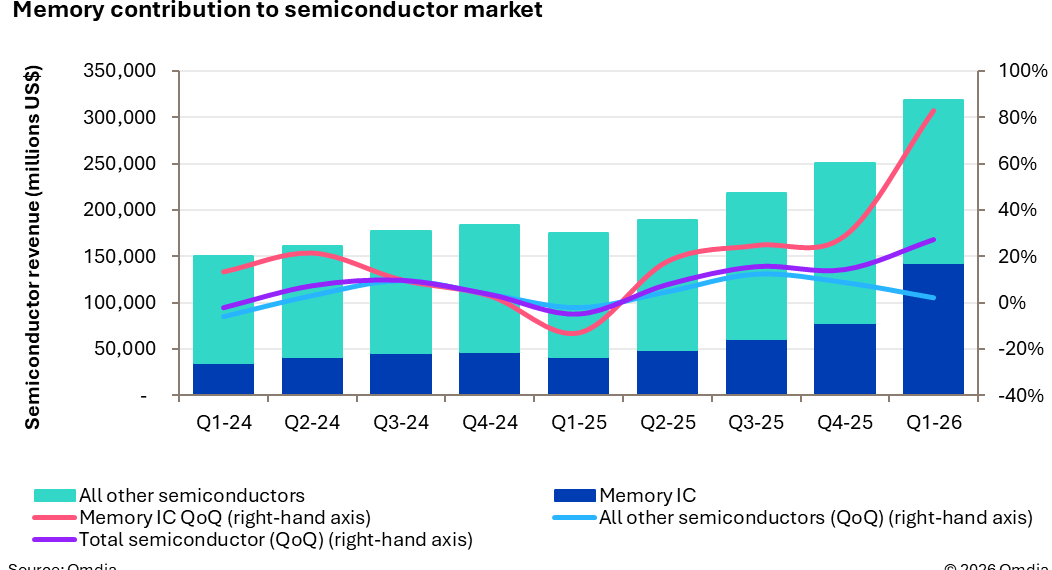

Memory has emerged as the defining force behind the surge. Combined DRAM and NAND revenue nearly doubled in a single quarter, reflecting a sharp tightening of supply conditions alongside aggressive price increases. Together, memory products accounted for more than 40% of total semiconductor revenue in 1Q26, significantly above the long-term average of around 20%.

NAND flash was the standout segment. Revenue climbed to just under $48 billion, rising 96% quarter-on-quarter. Prices increased nearly in lockstep, with average selling prices up 95% during the period. Omdia attributes the momentum to sustained AI-driven storage demand, persistent supply constraints, and limited output flexibility as manufacturers navigate technology transitions and yield optimization challenges.

Supply-side conditions remain tight across much of the memory ecosystem, with high utilization rates and gradual recovery cycles limiting capacity expansion. As a result, pricing strength is expected to persist into the second quarter, supporting continued revenue gains.

Outside of memory, semiconductor performance followed a more traditional seasonal pattern. Excluding memory integrated circuits, the broader market grew just over 2% quarter-on-quarter in 1Q26. This contrasts with historical trends, where the first quarter typically sees a decline of around 4%.

Several mature categories, including microcontrollers, discrete components, and optical devices, recorded expected seasonal declines. However, this weakness was offset by stronger-than-usual performance in AI-related chips and data center infrastructure components, which helped lift the non-memory segment into modest growth territory.

The divergence underscores a growing structural split in the semiconductor industry. On one side, AI and data center demand is accelerating high-performance segments. On the other, traditional components continue to reflect cyclical and seasonal dynamics.

Looking ahead, Omdia expects growth momentum to continue in 2Q26, although at a slightly slower pace. Even so, the market is projected to deliver sequential growth exceeding 20%, driven primarily by memory.

“Four consecutive quarters of double-digit revenue growth for the market show the strength of the current demand for semiconductors,” said Clifford Leimbach, Practice Leader at Omdia. He noted that the current trajectory places the industry on course to surpass $1 trillion in annual revenue within the year.